A breakdown of traditional property investing versus co-living, why the old model is under pressure, what investors need to understand about cash flow and yield, and how to avoid the costly mistakes most newcomers make.

Australia’s property investment landscape is undergoing a fundamental shift. Rising interest rates, inflated purchase prices, and tightening lending conditions have squeezed the traditional buy-and-hold residential strategy to the point where many aspiring investors are being locked out entirely. But a new model purpose-built co-living investment is challenging much of what we thought we knew about how to build a property portfolio.

This article unpacks the old way versus the new way of investing in residential land, examines why well-located co-living properties are generating yields significantly above the market average, and explains what separates the investors who succeed in this space from those who make costly mistakes. Whether you’re a seasoned investor or exploring property for the first time, this is a conversation worth having.

The Old Way of Property Investing: Why the Traditional Model Is Under Pressure

For decades arguably the better part of a century the conventional Australian property investment strategy has followed a simple formula: buy a residential home, find a tenant, hold the asset, and rely on capital growth over time. It’s a strategy built on patience, and for many investors over the past few generations, it worked.

But that model carries an almost unavoidable cost: negative cash flow. In practical terms, this means the rental income your investment property generates is not enough to cover the mortgage repayments and holding costs. You’re topping up the difference out of your own pocket, counting on the property’s long-term capital appreciation to make you whole.

For years, when interest rates were historically low and property prices were more accessible, investors could absorb this cost. But that window has effectively closed.

The Perfect Storm: Interest Rates, Migration, and a Supply Crisis

Over the past five years, a confluence of forces has dramatically inflated residential property prices across Australia’s major markets. Pandemic-era government stimulus schemes, record levels of migration, and suppressed construction activity have driven demand to extraordinary levels while supply has barely kept pace.

At the same time, the interest rate environment has reversed sharply. The holding costs of investment properties have surged, household living expenses have risen, but wages have not kept up. The margin investors had to comfortably absorb negative cash flow has been “squeezed pretty dramatically,” as one experienced property investment advisor puts it.

The consequences are significant. Not only are existing investors under pressure, but fewer new investors can enter the market at all. People who could have comfortably considered an investment property just a few years ago are now priced out and that means fewer new homes are being built as investment properties, which only deepens the housing supply crisis.

The old model doesn’t just hurt investors, it’s bad for renters, bad for housing affordability, and ultimately bad for the broader economy.

The New Way: Co-Living Investment Properties Explained

So what exactly is the “new way”? It’s co-living investment and while the concept is gaining momentum across Australia, it remains misunderstood by the majority of investors.

On the surface, a co-living investment property looks just like the house next door. From the street, there’s nothing to distinguish it from a standard residential home. But inside, it has been purpose-built to accommodate multiple independent residents, each with their own private suite. Instead of renting the whole dwelling to one family or tenant, the owner rents individual suites typically between three and nine to separate residents, each paying their own rent.

For comparison: Floorplan of a purpose-built co-living dwelling with private suites.

What a Co-Living Suite Actually Looks Like

This is where purpose-built co-living diverges sharply from a traditional share house. Each suite in a well-designed co-living property typically includes:

- A private bedroom and ensuite bathroom

- A kitchenette within the suite itself

- Potentially a private courtyard or outdoor space

- Individually lockable access residents are not reliant on others for their personal space

- Access to shared communal areas that are centrally managed

The design philosophy is critical. Residents aren’t forced to share a bathroom or navigate kitchen politics with strangers. They have their own retreat, their own space, their own life while benefiting from the security of a well-managed community environment. Anecdotal experience and operator data suggest household harmony is measurably higher than in a traditional share house, which translates directly into better tenant retention and stronger achievable rents.

The Numbers That Are Turning Heads: Co-Living Yields vs Traditional Investment Returns

This is where co-living investment becomes genuinely compelling.

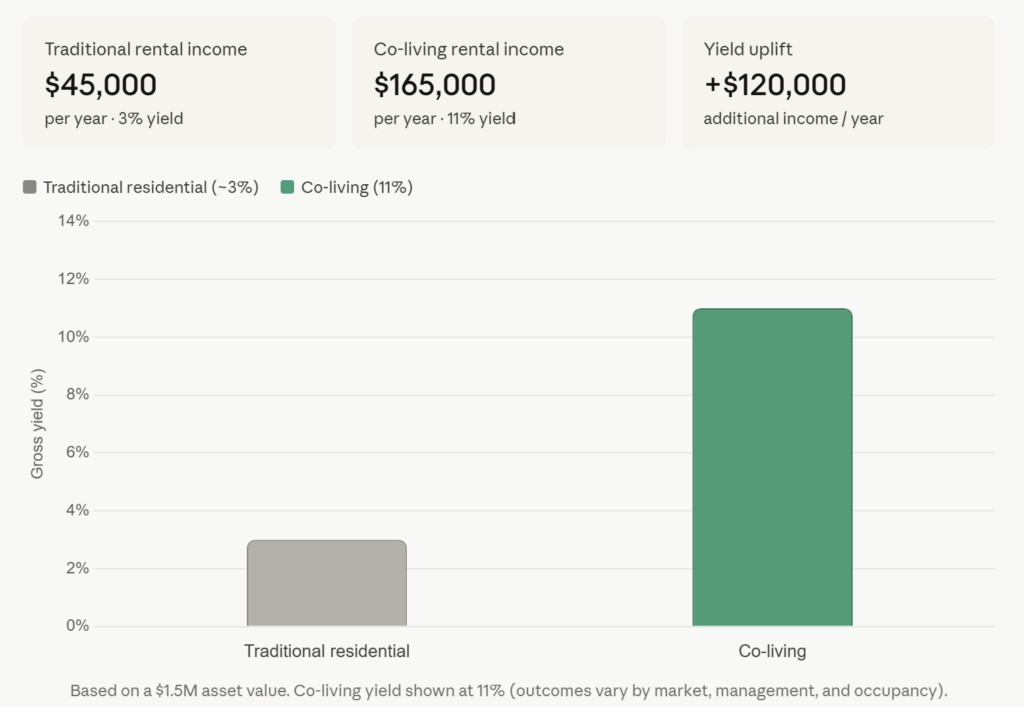

Consider a $1.5 million investment property in a major Australian city Brisbane, Sydney, or Perth. A traditional investment property at this price point might generate a gross rental yield of around 3%, or approximately $45,000 per year. That’s before mortgage repayments, rates, maintenance, property management fees, insurance, and vacancy periods. In the current interest rate environment, that property is almost certainly cash flow negative potentially to the tune of several hundred dollars a week.

Now consider a purpose-built co-living property at the same $1.5 million price point. With individual suites renting (in well-located, well-specified examples) at between $380 and $550 per room per week, and between three and nine suites in the dwelling, the same total investment can generate annual rental income materially higher than a single-let asset in our experience, gross yields above 11% are achievable for well-designed properties in the right markets .

That’s not theoretical; these numbers are being achieved by investors who have built co-living properties to the right specification, in the right locations, with the right property management behind them. They are not, however, guaranteed. Yields depend on location, build quality, suite design, market conditions, and management.

Gross yield comparison: traditional vs. co-living investment property in Australia.

1 Yield figures referenced in this article are based on internal portfolio data and observed market performance for purpose-built, well-located, well-managed co-living properties. They are illustrative, not forecasts, and individual property performance varies. Substantiate with internal data or independent third-party research before publication.

What Drives Rent Per Room So High?

The answer lies in both supply and specification. Australian Bureau of Statistics census data consistently shows that a substantial proportion of households in metropolitan suburbs are single-person households. Industry surveys suggest a significant share of solo-living adults would consider a quality co-living arrangement but only if the product quality is high enough.

The demand pool is large. To house even a fraction of it, you’d need vastly more co-living supply than currently exists. The imbalance between demand and supply is why well-specified co-living properties maintain waiting lists and achieve full occupancy over extended periods.

Critically, there is significant price elasticity in what residents will pay. In markets where inferior co-living products struggle to achieve $200 to $250 per room, high-quality properties with premium specifications consistently achieve $400 and above. Product quality directly determines income.

2 Australian Bureau of Statistics, Census of Population and Housing household composition data. See https://www.abs.gov.au for the most recent release.

Why Positive Cash Flow Changes Everything for Property Investors

The shift from negative to positive cash flow isn’t just a financial metric; it fundamentally changes the investor’s relationship with their portfolio and their ability to grow it.

1. Lifestyle Impact: Your Property Works for You, Not Against You

When each investment property in a traditional portfolio costs $200, $300, or $400 a week to hold, those costs represent lifestyle decisions foregone. Family holidays, home improvements, discretionary spending all eroded by the obligation to service a negatively geared asset.

A positively geared co-living property reverses this equation entirely. Instead of feeding the portfolio, the portfolio feeds you. Surplus cash flow can be used to supplement income, accelerate mortgage repayment on your own home, or simply afford a higher quality of life.

2. Portfolio Scalability: The Exponential Effect

Real financial freedom through property almost never comes from a single investment. It comes from a portfolio of multiple properties compounding in value and generating cumulative cash flow. But building that portfolio requires borrowing capacity, and borrowing capacity requires demonstrable income.

Every cash-flow-negative property you add to a traditional portfolio reduces your assessed borrowing capacity. Each property makes the next one harder to acquire. Co-living investment flips this dynamic: every positively geared property you add strengthens your borrowing position, making lenders more willing to finance the next acquisition. Each property you buy makes the next one easier to buy creating an exponential portfolio-building effect that the traditional model simply cannot replicate.

3. Built-In Vacancy Diversification

One of the most underappreciated risks in traditional property investment is vacancy. When your single-tenancy investment property sits empty, your income drops to zero but your mortgage, rates, and insurance continue regardless. This can create acute financial stress, particularly in a high-interest-rate environment.

A co-living property with nine suites has inherent vacancy diversification built in. If one resident departs, you lose one-ninth of your income, not all of it. In practice, you’d still be generating eight-ninths of your peak rental income while finding a replacement, which in a well-managed property with a waiting list can happen almost immediately. Even in the highly unlikely scenario of losing three residents simultaneously, most well-structured co-living properties remain cash flow positive.

4. A Buffer Against Interest Rate Cycles

Interest rate cycles are an inescapable reality of property investing. Rates rise, rates fall, and investors who over-extend in the high-rate phase can find themselves forced to sell assets at the worst possible time under financial duress, often accepting below-market offers.

The substantial cash flow buffer that a co-living property generates acts as a financial shock absorber. Internal modelling on properties in our portfolio has shown that even with multiple consecutive interest rate rises, a well-structured co-living asset can remain cash flow positive. The excess yield created at the outset provides headroom that rate rises which would devastate a traditional investor barely registered.

That cash flow buffer transforms from enhancing your lifestyle in good times to protecting your portfolio in challenging ones. It means you are never forced to act, never compelled to sell at an inopportune moment, never negotiating from a position of desperation.

Want to model the cash-flow profile of a co-living investment in your situation? Book a 30-minute strategy call.

The Regulatory Framework: Why 1B Certification Is Non-Negotiable

One of the most critical distinctions between a genuine co-living investment and an informal share house arrangement is Class 1B building certification and this is an area where ignorance can be extraordinarily costly.

In Australia’s building classification framework, most residential homes fall under Class 1A. Commercial buildings, apartments, and larger-scale residential developments sit under Class 3. A purpose-built co-living property sits at Class 1B a deliberate middle category that imposes higher construction standards, fire safety requirements, and council approval processes.

The 1B certification creates some friction in the development process; it costs more to build, requires additional council dialogue, and takes longer to approve. But it delivers two critical outcomes:

- It future-proofs the investment: the property is fully compliant within the regulatory framework, protected against any future tightening of co-living regulations.

- It legally enables the co-living arrangement: without 1B certification, operating a multi-resident dwelling as a co-living property is at minimum a regulatory breach and, depending on jurisdiction, can constitute a criminal offence carrying potential custodial penalties.

This is one of the most important differentiators between a genuine co-living investment and an informal share house arrangement. A regular house with multiple tenants sharing costs is not a co-living property; it’s an unregulated arrangement that exposes the landlord to serious legal risk. (For the full breakdown of what 1B certification involves, costs, and how to obtain it, see our companion guide: What Is a 1B Certification? The Complete Guide for Co-Living Investors in Australia.)

Residents vs Tenants: A Legal Distinction Worth Understanding

In a Class 1B-certified co-living dwelling, occupancy arrangements are typically structured differently from a standard residential tenancy. The legal mechanism varies between Australian states and territories Victoria, NSW, Queensland and other jurisdictions each take a slightly different approach to short-stay, rooming-house, and shared-accommodation legislation . In some structures, occupants may be governed by different legislation than a standard tenancy, which can affect notice periods, dispute resolution, and the enforceability of house rules.

The practical upshot is that, depending on the structure used, landlords can have a more workable framework for maintaining standards in a multi-resident environment including documented house rules residents agree to upon entry. House rules must be reasonable and mutually agreed upon; they’re not a mechanism for arbitrary restrictions. They provide a contractual framework for community standards that complements (rather than replaces) the underlying legislation.

This is genuinely state-specific and structure-specific. Get specialist legal advice on the framework that applies to your property.

The Most Common Mistakes Co-Living Investors Make (and How to Avoid Them)

Co-living investment done well is genuinely transformative. But there are identifiable patterns of error that consistently harm investors who enter the space without proper guidance.

Mistake #1: Prioritising Cheap Land Over Good Location

The most common error is attempting to reduce the upfront investment by purchasing the cheapest available land and assuming the co-living strategy will make the numbers work regardless of location.

It won’t. Land is cheap for a reason usually because it lacks the infrastructure, transport connectivity, and lifestyle amenity that makes a location attractive to the kind of quality tenant a premium co-living property needs to attract. A $200,000 block in a poorly serviced location with an $850,000 build on top of it is both a poor co-living investment (because you can’t attract quality tenants or achieve premium rents) and a poor capital growth play (because the value is almost entirely in the depreciating building, not the appreciating land).

The location selection for a co-living property should be approached with virtually the same rigour as selecting a traditional residential investment. You want tightly held, well-connected suburbs with demonstrated rental demand, quality infrastructure, and strong long-term capital growth fundamentals. The co-living format multiplies the income from that land; it doesn’t substitute for the land’s quality.

3 Residential tenancies and rooming-house legislation varies materially by state. Refer to: Residential Tenancies Act 1997 (Vic), Residential Tenancies Act 2010 (NSW), Residential Tenancies and Rooming Accommodation Act 2008 (Qld), and equivalents in other states.

Mistake #2: Building to a Minimal Specification

Given the higher build costs associated with co-living (due to the 1B certification requirements and the need for individual suites), some investors attempt to recover margin by cutting the quality of the fitout. This is a false economy that directly undermines the investment’s income-generating potential.

Remember: the demand side responds to quality. A basic, institutional-looking property with cheap finishes will attract the bottom of the market with the rents and behaviours that come with it. A well-specified, beautifully presented co-living property can attract professionals, downsizers, and quality long-term residents who will pay premium rents and stay for years.

The best operators in this space build to a specification that rivals and in some cases exceeds the quality of a standard owner-occupied home. Beautiful bathrooms, well-appointed kitchenettes, private outdoor spaces, high-quality shared areas. The cost difference at build stage is a fraction of what the income difference delivers over a 10- or 20-year investment horizon.

Mistake #3: Using the Wrong Property Manager

This is perhaps the most fixable of the major mistakes but also one of the most consequential. Co-living property management is a specialist discipline. A standard residential property manager, however competent, does not have the systems, processes, or experience to manage a multi-resident 1B dwelling effectively.

The issues that arise in a co-living property are different from those in a standard rental. Managing house rules, maintaining community harmony, handling individual lease agreements, and most critically maintaining full tenancy through proactive vacancy management all require specialist know-how.

The best co-living property managers maintain continuously active vacancy listings even when a property is fully occupied. When a resident gives notice, they’re not starting the leasing process from scratch they’re selecting from a pre-screened waiting list. Cleaners come in the day the room becomes available; the new resident moves in the following day. Zero vacancy, zero disruption, zero lost income.

When assessing a co-living investment, be cautious of seeking advice from general real estate agents. They often lack the knowledge to properly appraise a co-living property and may steer you away from the concept simply because they don’t want to manage it. Seek out property managers who work exclusively or predominantly in the co-living space, have demonstrable track records, and can provide independently verifiable occupancy and rental rate data.

Mistake #4: Not Setting House Rules at the Outset

For investors who do proceed with a co-living property, one of the most easily avoided yet surprisingly common errors is failing to establish documented house rules from the outset.

Properly drafted, mutually agreed house rules give landlords a workable framework for maintaining community standards but only if they are formally documented and signed at the point of entry. Without them, landlord rights revert to the base legislation, which (as with standard tenancy law) is heavily weighted toward protecting the occupant.

Isn’t Co-Living Just a Yield Play? What About Capital Growth?

A fair question and one worth addressing directly, because it gets to the heart of why co-living investment is genuinely superior to most alternatives, not just a trade-off.

The capital growth potential of a co-living property is not diminished by its income characteristics provided the location selection is done correctly. The investment still sits on residential land in a well-chosen suburb with all the fundamentals that drive long-term appreciation. Unlike commercial property, which is priced and valued primarily on its income yield, residential land in strong-growth corridors appreciates based on supply-demand dynamics, infrastructure development, and population growth.

The co-living format delivers superior cash flow without sacrificing capital growth. It’s not an either/or proposition, it’s both. This is a fundamental structural advantage over commercial property investing, where high yields typically come at the expense of land value appreciation.

More to the point, the cash flow the co-living property generates during the holding period allows investors to hold through the inevitable market cycles, interest rate peaks, rental market fluctuations, economic downturns without being forced into distressed sales at the worst possible moment. It’s the cash flow that preserves the capital growth story, because it means you can always afford to wait for the right time to sell.

Co-Living Investment as a Solution to Australia’s Housing Crisis

There’s a dimension to co-living investment that goes beyond the personal financial case and it’s one that gives this strategy genuine social and economic legitimacy.

Australia is in the midst of a housing crisis. Supply is insufficient. Rents are unaffordable for a growing proportion of the population. New construction is failing to keep pace with demand. Traditional investment property ownership has become inaccessible to many, reducing the pipeline of new supply from the private sector.

Co-living investment addresses several of these failures simultaneously. It creates new, high-quality housing supply. It provides affordable, well-serviced accommodation to a segment of the population that is dramatically underserved by the current housing stock. And it does so in a way that is commercially sustainable for the investor meaning it will attract private capital at scale in a way that government programs and social housing simply cannot.

The reason co-living is good for investors is fundamentally because it’s good for residents. It meets a genuine, urgent need in the market. That alignment between investor returns and social outcomes is rare and it’s one of the reasons this model is attracting increasing attention from sophisticated investors across the country.

Key Takeaways: Old Way vs New Way at a Glance

Traditional residential investment:

- Typically negative cash flow costs money each week to hold

- ~3% gross yield in most major markets at current prices

- Reliant on long-term capital growth to generate returns

- 100% vacancy risk lose one tenant, lose all income

- Each property makes the next harder to finance

- No regulatory differentiation from owner-occupied homes

Co-living investment (done correctly):

- Positively geared generates surplus cash flow from day one

- Materially higher gross yield achievable with the right specification and location

- Delivers both yield and capital growth from residential land

- Inherent vacancy diversification losing one resident has minimal income impact

- Each property strengthens borrowing capacity and accelerates portfolio growth

- 1B certification provides regulatory certainty and structured tenancy frameworks

- Purpose-built design extracts premium rents and delivers superior tenant retention

Is Co-Living the Future of Australian Property Investment?

In an environment where traditional residential investment has become financially unsustainable for many and structurally problematic for the broader economy, co-living investment offers a better answer for investors, for residents, and for the housing market as a whole.

It isn’t easy to do well. Getting the location right, the specification right, the regulatory compliance right, and the property management right requires knowledge, diligence, and access to specialist expertise that most investors don’t have by default. The investors who cut corners on land quality, build quality, or management quality consistently underperform.

But the investors who approach co-living investment properly with the right advice, the right team, and the right long-term mindset are building portfolios that generate real cash flow, sustain themselves through economic cycles, and appreciate in value over time. They’re not waiting for interest rates to fall or capital growth to bail them out. Their portfolios are working for them right now.

If you’re evaluating your property investment strategy and asking whether there’s a better way there is. The next step is to look at it through the lens of your own situation and decide whether the model fits your goals, your timeline, and your appetite for getting it right from day one.

Book a 30-minute strategy call with our team no obligation, and we’ll tell you straight whether co-living fits your situation.

Related Reading

- What Is a 1B Certification? The Complete Guide for Co-Living Investors in Australia

- SMSFs and Co-Living Properties: Building Tax-Effective Retirement Wealth

Disclaimer: This article is intended for general informational purposes only and does not constitute legal, financial, or construction advice. Always consult a registered building surveyor, licensed builder, qualified financial adviser, and where applicable a property lawyer before making investment decisions.